What are International Surety Bonds? Well that depends on where you call home. Although we have customers and readers around the world, our headquarters is in the United States. This article writes international surety bonding from that perspective. International surety bonds include a wide variety of common surety bonds including the following:

• Construction Bonds – Bid Bonds, Performance Bonds and Payment Bonds

• Maintenance Bonds

• Supply Bonds

• Custom Bonds

• License and Permit Bonds

• Advanced Payment Bonds

• Court Bonds

• Financial Guarantees

• Specialized Contract Bonds – Specific to each country

Writing International Surety Bonds from a U.S. perspective takes place primarily in two forms. The first is bonds written by U.S. based companies in foreign countries. The second is referred to as “Reverse Flow”. Reverse Flow is when a foreign corporation needs to provide surety bonds in the United States.

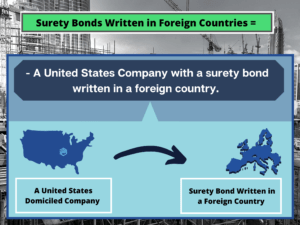

Bonds Written in Foreign Countries

An example would be a construction contractor located in Dallas, Texas who needs a performance bond for a contract in Madrid, Spain. This is the more complicated of the two types of international surety bonds discussed. Let us look at the reasons why.

Foreign Law

For a project in a foreign country, the contract is likely written in the laws of that country. Surety law in the United States is very old. Case law had determined a surety companies rights and responsibilities many times over in the United States and company underwriters are familiar with those laws and can reasonably determine an outcome in both contract disputes and surety bond claims. That may not be the case in a foreign country. For many countries this is not an issue, but surety bond companies want to be very comfortable with the local laws and regulations before writing bonds in a foreign country.

Advanced Payment Bonds

In some foreign countries, funds are advanced to the contractor upon signing a contract. The intent is for these funds to be used for the project. Advanced Payment Bonds protect the Owner by guaranteeing that those funds will be used for those purposes. Often a separate Advanced Payment Bond is issued with each payment to the contractor creating separate liabilities to the surety bond company. This contrasts with construction practices in the U.S. where contractors are usually not paid until after the work is complete. These bonds are usually forfeiture bonds which are higher risk to the surety bond company.

Experience

A key underwriting question will be why the Principal is doing this international project. Are they a large multinational corporation who regularly works in foreign countries or will this be there first project in that country? Do they have offices and staff in that country? Do they have local labor? Do they understand the local political climate? Understanding the answers to these questions will be key to getting a surety bond approved.

Uniqueness of Product or Experience

Like the last point, is uniqueness of product and/or experience. When underwriting these surety bonds in foreign countries, a surety bond company will want to know why this project makes sense for the Principal. Does a company have a specialty product, with few competitors around the globe? An example may be a company who supplies and installs amusement park rides. Instead of a product, it may be specialized experience. Not every contractor can build large scale treatment plants, power generating facilities, ect. Those that do may find the best opportunities in foreign countries.

On the other hand, if a company does not have a unique product or experience, the surety bond company is going to question why the project makes sense. For example, why would a general contractor travel to a foreign country to build an apartment complex? Why would an owner choose them over the many local companies that are qualified to build the same project? Expect the surety bond company to be very skeptical of these situations.

Mobilization and Demobilization Costs

For construction companies, the cost of mobilizing to a foreign country is extremely expensive. How these project costs will be handled is very important. Getting people, material and equipment overseas is not only expensive but it can also be quite a logistical challenge. Contractors need significant experience is handling this risk. I have seen instances where contractors can only get supplies via cargo ship once per month. That means additional supplies or unplanned equipment breakdowns are not only expensive, but they can cause significant delay costs. Finally, what about demobilization? What do you do with left over equipment and supplies? Having to unexpectedly ship items back to the U.S. can eat up job profits.

Difference in Contract Language

Contract terms mean different things in different languages. In the United States, Performance Bonds are a three-party agreement between a Principal (Company Providing the Bond), Obligee (Bond Beneficiary) and Surety (The Bond Company). To make a claim on a performance bond, the oblige must fulfill their obligations including payment. However, in many foreign countries, contracts that require a performance bond are looking for something different. They often want a straight financial guarantee or a forfeiture bond that can be called on demand. Surety bond companies will usually only write these for the strongest of Principals with significant net worth. These requirements are usually better served with an Irrevocable Letter of Credit at an acceptable bank.

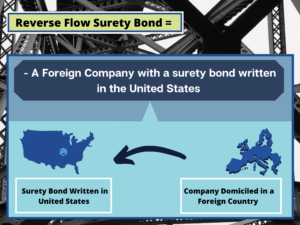

Reverse Flow International Surety Bonds

The second type of international surety we will discuss is Reverse Flow. An example of this would be a construction contractor from Madrid, Spain needs to provide performance and payment bonds for a project in Dallas, Texas. As mentioned, reverse flow is the easier of the two types but presents its own unique underwriting considerations. These include the following.

Indemnity Agreement

In reverse flow situations, the project location and contract are in the United States, so they surety bond company is comfortable with the venue. However, surety bonds are a product of indemnity and the surety bond company expects the Principal to reimburse them if they incur a loss. This can be tricky with foreign entities. Surety bond underwriters will want to make sure that their indemnity agreement will be enforceable against the Principal in the event of a loss. Researching local laws and creating indemnity agreements in foreign countries is very expensive. Therefore, surety bond companies will typically only file new indemnity agreements for very large companies who have the potential to generate significant surety bond premium. Fortunately, as the World becomes smaller and more international business takes place, more surety bond companies are creating indemnity agreements in more countries. Countries with established indemnity agreements and surety laws make getting these reverse flow surety bonds much easier. If the Principal operates in a country with these agreements in place, they need to be able to generate significant premium to make it worthwhile for the surety bond company.

A second issue with Indemnity Agreements is that some countries consider an indemnity agreement to be an obligation that shows up on the company’s financial statement as a liability or contingent liability. This may impact the company’s other credit relationships. One potential compromise is for the surety bond company to limit indemnity to a specific dollar amount. However, surety companies will only do this if the Principal if very strong and overqualified for the surety bond credit needed.

United States Operations

One way to make getting reverse flow surety bonds significantly easier for the Principal is to have a base of operations and financial assets in the United States. Having assets in the U.S. makes it easier for surety bond company to lend surety credit against those assets. If a problem arises, its easier to seek reimbursement from U.S. assets than foreign assets.

Collateral

For companies without U.S. based assets, and/or where indemnity agreements are not readily available, collateral may be required. In these situations, the collateral requirements are usually an Irrevocable Letter of Credit at a U.S. based bank. The collateral amount required depends on the situation.

Net Worth Requirements for All International Bonds

For both surety bonds written in foreign countries and reverse flow surety bonds, the Principal needs to be able to qualify financially. For most surety bond companies, the standards are higher for companies looking to do international work. Because these surety bonds have more risk, the bond Principal needs extra financial cushion to even be considered. In fact, many surety bond companies will not consider writing International Surety Bonds for companies unless their net worth is eight figures or more. Of course, there are always exceptions for the right circumstances. Although international surety bond options are improving, companies with smaller balance sheets can expect hurdles obtaining these surety bonds and may have to post collateral to get them.

International Surety Bonds can be complicated. By understanding the risk factors and having an appropriate plan in place, companies can make getting these surety bonds easier. Contact MG Surety Bonds anytime. We are surety bond experts!