In this article, we answer some of the most frequently asked questions about surety bonds. Surety bonds can be confusing, and MG Surety Bonds is here to make the process easier.

What is a Surety Bond?

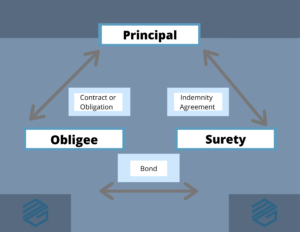

A surety bond is a three-party guarantee between a Principal (party making the promise) the Obligee (party receiving the guarantee) and a Surety (the bond company guaranteeing the Principal’s performance. There are many different types of surety bonds, but they fall into two general categories. These include Contract Surety Bonds and Commercial Surety Bonds.

1. Contract Bonds are a general term for construction related surety bonds. The main surety bonds that fall into this category are Bid Bonds, Performance Bonds, Payment Bonds and Maintenance Bonds. Developer Bonds usually fall into this category as well, but some surety bond companies view them as Commercial Surety. Construction Surety Bonds are required on all Federal projects over $150,000 because of The Miller Act. Most states and municipalities have similar requirements although the amounts may vary. They can also be required on private projects.

2. Commercial Surety Bonds are the second category. Commercial Surety includes many subcategories such as Court Bonds, License Bonds, Permit Bonds, ICC Freight Broker Bonds, Public Official Bonds, Oil and Gas Bonds, Financial Institution Bonds, Customs bonds and even Bail Bonds (The only type MG Surety does not write).

How Do Surety Bonds Differ from Insurance?

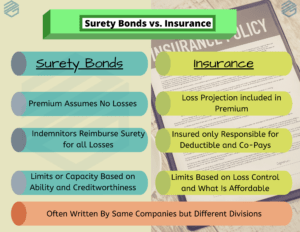

Surety Bonds are not insurance. Unfortunately, there is much confusion on this and for good reason. After all, surety is typically regulated by each state’s Department of Insurance. In most states the legal requirement to sell surety bonds is a property and casualty insurance license. Additionally, many of the largest surety bond writers are also some of the largest writers of property and casualty insurance. With so much overlap, it’s easy to see why surety bonds could be mistaken for an insurance product. Surety is more closely related to a credit product such as banking.

Consider that surety is an indemnity product. That means that before getting a surety bond, the Principal will be required to sign a General Indemnity Agreement. This agreement spells out the Principal(s)’ obligations to the surety bond company. One of those obligations is always to reimburse the surety bond company for any losses they may occur. Although losses do happen, surety bonds are written with anticipation of no losses. This makes the product affordable and typically keeps surety bond rates to less than 3% of the obligation. Pricing losses into surety bond premiums would make the costs to expensive. This is in stark contrast to property and casualty insurance. The owner of an insurance policy is usually only responsible for a deductible and maybe co-insurance. The remainder of the loss belongs to the insurance company. These policies are written and priced with the assumption of some losses, and this is typically between 20%-40%. These losses are priced into the premiums.

Surety Bonds and insurance are underwritten much differently. Insurance is mostly concerned with safety and loss control to prevent future claims. Surety underwrites the Principal’s finances, character, and capabilities to complete an obligation. The surety bond company gives them a credit limit called “Capacity” and allows them to work within that limit. This is different from insurance where an insured can often purchase limits as high as they can afford. Regardless of who you work with, make sure you work with an expert for your surety bond needs and an expert for your insurance needs. I can tell you that many people sell both products, but few are experts at both.

How Do You Get a Surety Bond?

That really depends on the type of surety bond, the amount of the guarantee, and the length of the obligation. Small contract surety bonds can usually be written with a short credit application while larger contract bonds need to go through full surety bond underwriting, often referred to as “The 3 C’s”. Many license and permit bonds are written freely and do not require any underwriting. Other commercial surety bonds such as Tax Bonds are a financial guarantee and typically require financial statements on both the company and the owners. Some surety bonds may even require collateral because of the type of risk. Each type of surety bond has its unique requirements.

What Kind of Financial Statements are Required to Get a Surety Bond?

There is no hard and fast rule for this. Each surety bond company has their own unique underwriting standards. In general, the larger the surety bond or bond program, the more sophisticated the financial statements need to be. Small surety bonds can be written with no financial statements. Some can be written with internal statements or tax returns. Others may require a CPA Compilation, Review or even an Audit depending on the size. You can read more about financial statement requirements here.

Can I Get a Surety Bond with Bad Credit, Bankruptcy, Judgments or Liens?

In general, yes but it depends on the circumstances and the type of surety bond. For commercial bonds, often it is just a matter of rate. For contract bonds, it will depend on other factors including the financial strength of the company. The SBA Surety Bond Guarantee Program will guarantee contract surety bonds for those with bankruptcies, liens and judgements so long as they are discharged, satisfied or a payment plan is in place. Open tax liens present a problem for all types of surety bonds as nobody wants to be a creditor behind the government. For other non-contract bonds, there are alternatives such as collateral, or funds control that can help a more difficult situation.

What Do Surety Bonds Cost?

Again, it depends on several factors and the type of surety bond requested. A typical range is between 0.5% to 3% of the bond amount. This varies depending on many factors. In general, the stronger the account, the lower the rate. For contract bonds, you can read all about rates here. Contract surety bonds are usually written on a sliding scale so that the rate decreases as the contracts increases. With commercial surety bonds rates can also be less than 1% but may be as high as 10% for those with challenging credit. In commercial surety, bond companies often give discounts for purchasing multiple years upfront.

Why Does My Spouse Have to Sign the Indemnity Agreement?

As we said above, surety is an indemnity product. That means the surety bond company expects to be reimbursed in the event of a loss. Depending on the indemnity agreement, the surety bond company may seek reimbursement from the company and/or the owners and other indemnitors. If an owner indemnifies, a spouse will be expected to as well. This prevents a party from sheltering assets, or shifting them to a spouse. This is usually the case even if the spouse has no ownership in the business. There are exceptions to this rule, but they are rare.

Why Do My Other Businesses Have to Sign the Indemnity Agreement?

This occurs for a couple of reasons. One, the surety bond underwriter may be relying on the assets of the other business to extend surety bond credit. Additionally, this is to prevent the shifting of assets in a claim scenario. Exceptions can be made if the circumstances qualify.

Can Surety Bonds Be Cancelled?

It depends on the type of surety bond. Contract bonds such as bid bonds, performance bonds, payment bonds and supply bonds cannot be cancelled once issued. If it is determined that they are not needed, the original bonds must be returned to the surety before a refund can be issued. Commercial bonds such as license and permit bonds can usually be cancelled. However, some do have time requirements such as 60 days’ notice. Others may even require that the Obligee consent before cancelling. There are other types that require the surety bond to be replaced by another surety bond and bond company before they can be cancelled.

How Do I Get Off the Liability on Construction Bonds?

Construction bonds do not need to be canceled. The guarantee simply expires as the obligation is complete. For example, there is no need to return a performance bond or a payment bond. Once the project is complete and the bills are paid, there is no further obligation. The same can be said of bid bonds and maintenance bonds. The protection on the surety bond stays in place until the obligation is complete. Obligees to not typically return these surety bonds as it is unnecessary.

Why Use a Surety Bond instead of a Letter of Credit?

Many obligees will allow you to post a letter of credit instead of a surety bond. There may be reasons not to do this though. Surety bonds are generally considered unsecured credit so that they will not tie up your resources. Posting letters of credit on the other hand will reduce your borrowing ability. For most Principals, surety bonds cost less than 3% while most letters of credit have a variable rate. Finally, surety bond companies are generally required to investigate claims before paying, while letters of credit have no such provisions. A claim, valid or not may be paid out under a letter of credit. You can read more about surety bonds versus letters of credit here.

What are Overruns and Underruns?

In Contract Surety, the premium is based on the final contract amount. That could be more or less than the original contract amount. Many surety bond companies send out Contract Status Reports to the Obligee throughout the course of the project and at the end. The Principal may owe additional premium if the final contract was more than the original contract. This is called an Overrun. The final contract could also be less than the original contract amount. In this case, the surety bond company owes money back to the Principal. This is called an Underrun.

What is a Surety Bond Dividend?

Some states such as Texas have a dividend plan. The contractor pays the surety bond premium up front on construction bonds and is eligible for a dividend from the surety bond company at the end of a project.

What is the Difference in Surety Bond Companies?

There are many different surety bond companies. In fact, there are over 100 operating in the United States alone. Each company has a slightly different underwriting appetite although there is quite a bit of overlap. We work with many different surety bond companies to find the best fit for each customer. We believe that regardless of the company, they should be a corporate surety that is listed “A-“ or better by a credible rating agency such as A.M. Best. In most cases, we believe they should also be listed on the U.S. Treasury’s 570 Circular as this is required by most contracts.

What is the Difference in Surety Bond Brokers?

Unfortunately, almost anyone can get licensed to write surety bonds. Most states only require a property and casualty insurance license. Obtaining an insurance license requires virtually no understanding of surety, financial statements or business operations. Therefore, the barriers to entry are very low and many surety bond brokers are run by those with backgrounds in contractor digital marketing or insurance. We encourage customers to work with surety bond experts, even if it is not us. Look for those brokers that are part of the NASBP or have AFSB designations. These brokers usually have a background in surety bonds and will make getting your bonds easier. In fact, many of our customers have been turned down by these other brokers first.

Your Surety Bond Questions Answered

We are always updating our list of surety bond frequently asked questions. Feel free to contact us anytime and we can help you over the phone, through email or through this page. We look forward to helping you with your surety bond needs.